%20(4).png)

Contact

Find us

- RCK Partners,

70 Gracechurch Street,

London,

EC3V 0HR.

© 2024 RCK Partners - Company House No: 12396021

.jpg)

Last updated: June 2026

We spoke with Anastasiya Kokonova, Capital Allowances Partner at RCK Partners, to explain how Research and Development Allowances (RDAs) work in practice, which capital costs can qualify, how RDAs interact with R&D tax relief and Structures and Buildings Allowance (SBA), and how businesses can maximise available tax relief on innovation-related expenditure.

Research and Development Allowances (RDAs) are a form of capital allowances that provide 100% tax relief on qualifying capital expenditure incurred on assets used for carrying out qualifying research and development (R&D) activities.

Unlike R&D tax relief, which generally applies to revenue expenditure such as staff costs and consumables, RDAs apply to capital expenditure on buildings, facilities, equipment and infrastructure used for qualifying R&D activities.

The relief allows businesses to deduct the full qualifying expenditure from taxable profits in the year the expenditure is incurred, significantly accelerating tax relief and improving cash flow.

Research and Development Allowances can apply to a wide range of capital expenditure incurred on assets used directly for qualifying R&D activities.

Examples include:

In some circumstances, expenditure on buildings used for qualifying R&D activities may also qualify for RDAs.

The key requirement is that the expenditure is incurred on assets used for carrying out qualifying R&D activities seeking an advance in science or technology.

Research and Development Allowances are a specialist form of capital allowances designed specifically for capital expenditure incurred on qualifying R&D activities.

While other capital allowances such as Annual Investment Allowance (AIA), Full Expensing, First Year Allowances (FYA) and Writing Down Allowances (WDA) apply to qualifying plant and machinery, RDAs can extend to certain buildings and facilities used for research and development.

The main advantage is that qualifying expenditure attracts 100% tax relief in the year it is incurred, allowing businesses to accelerate tax relief compared to many other capital allowances regimes.

Yes. In many cases businesses can claim both Research and Development Allowances and R&D tax relief on the same overall project.

Generally:

For example, a company constructing a new testing facility may claim RDAs on qualifying capital expenditure while separately claiming R&D tax relief on qualifying staff costs, software, consumables and subcontractor expenditure.

A coordinated review ensures businesses maximise all available innovation-related tax incentives.

Any company carrying out qualifying R&D activities may potentially claim Research and Development Allowances.

Common sectors include:

The relief is available to businesses of all sizes, from start-ups and scale-ups through to large multinational companies.

The key test is whether the expenditure relates to assets used for carrying out qualifying R&D activities.

Yes. Research and Development Allowances can be particularly valuable where companies invest in laboratories, testing facilities and pilot plants used for qualifying R&D activities.

Many businesses assume buildings never qualify for capital allowances. However, where facilities are used for carrying out qualifying R&D activities, expenditure on those facilities may qualify for 100% Research and Development Allowances.

This can generate significant tax savings for businesses investing in innovation, product development and scientific research.

This is one of the most valuable aspects of Research and Development Allowances.

Ordinarily, expenditure on commercial buildings qualifies for Structures and Buildings Allowance (SBA), which provides tax relief at a rate of 3% per annum over approximately 33 years.

However, where qualifying facilities are used for research and development activities, certain expenditure may instead qualify for Research and Development Allowances at 100%.

This can accelerate tax relief dramatically, allowing businesses to obtain immediate relief rather than spreading deductions over several decades.

For companies investing in laboratories, research centres, testing facilities and specialist development buildings, the difference can be substantial.

Yes. Research and Development Allowances are not limited to newly constructed facilities.

Where expenditure is incurred refurbishing, extending or adapting existing facilities for qualifying R&D activities, the expenditure may potentially qualify for RDAs, subject to the statutory conditions.

This is particularly relevant for manufacturing businesses, agricultural companies and industrial operators that regularly modify or upgrade existing facilities to support ongoing research and development projects.

Each project should be reviewed on its own facts to determine the extent of qualifying expenditure.

Qualifying research and development equipment generally includes assets used directly in carrying out qualifying R&D activities.

Examples may include:

The equipment must be used for qualifying R&D activities rather than routine commercial production.

Establishing the extent of qualifying use is often one of the most important aspects of a successful RDA claim.

Many businesses focus solely on R&D tax relief and overlook the substantial benefits available through Research and Development Allowances.

To maximise relief, businesses should:

A detailed review often identifies qualifying expenditure that may otherwise be overlooked, helping businesses accelerate tax relief, improve cash flow and maximise the return on their investment in innovation and development.

A detailed review often identifies qualifying expenditure that may otherwise be overlooked, helping businesses accelerate tax relief, improve cash flow and maximise the return on investment in innovation.

Given the complexity of Research and Development Allowances legislation and the interaction with wider capital allowances and R&D tax relief regimes, specialist review is often essential to maximise claims while ensuring compliance with HMRC requirements. At RCK Partners, our experts combine capital allowances expertise with a detailed understanding of innovation-related tax reliefs, helping businesses identify qualifying expenditure and secure the maximum relief available.

Find out who can claim capital allowances in the UK, and which assets and property types qualify.

A step-by-step guide to making a capital allowance claim in the UK.

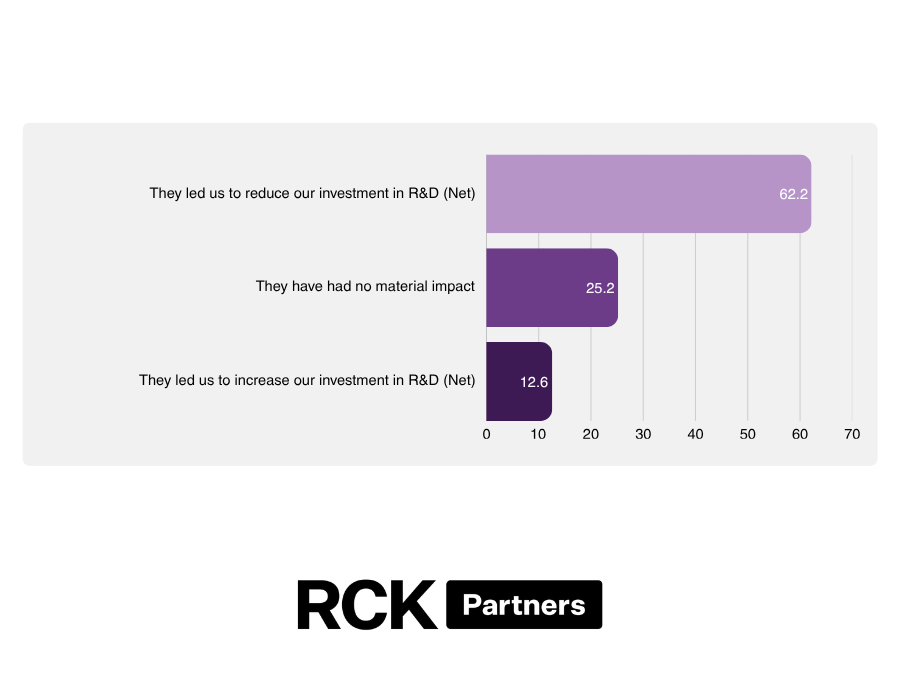

A Times-featured study, commissioned by RCK Partners and conducted by Censuswide, suggests that recent reforms to the UK's R&D tax relief scheme may have gone too far. The research found that measures introduced by HMRC to tackle abuse of the scheme are having unintended consequences for genuine innovators, with many businesses reporting that they have cancelled research initiatives, paused investment plans and reduced skilled headcount as a result of increased uncertainty surrounding the regime.