%20(4).png)

Contact

Find us

- RCK Partners,

70 Gracechurch Street,

London,

EC3V 0HR.

© 2024 RCK Partners - Company House No: 12396021

The report explores the UK's R&D scheme in relation to comparable schemes offered across other OECD countries and examines the effects of the UK's recent reforms to its R&D scheme. The focus is on the effects of the merged Research and Development Expenditure Credit (RDEC) and Small and Medium-sized Enterprises (SME) schemes, fully implemented in 2024. While these changes aim to reduce fraud and error and simplify the system, in reality, they have significantly reduced the R&D tax benefits available to SMEs. Given that SMEs account for the majority of R&D claims in the UK, this shift poses a substantial risk to the UK's innovation-driven growth. The UK has historically offered one of the most favourable R&D tax relief schemes, particularly for SMEs. However, introducing a merged scheme has raised concerns about its competitiveness. The report examines the impact of recent changes to the UK's R&D tax policies and their potential implications for the country's global competitiveness. While addressing fraud and error, the merged scheme has reduced overall tax relief for SMEs, the largest claimants by volume of R&D tax credits. Compared to Germany and Sweden, the UK now lags in GERD and BERD as a % of GDP, and this decline in SME support could risk further undermining the UK's attractiveness to investment in R&D.

Strengthening Compliance: To mitigate fraud and error while preserving the benefits of an R&D scheme, the government could adopt new or alternative compliance measures rather than cut tax relief. This approach would maintain the scheme's attractiveness for SMEs and ensure that genuine R&D activities are encouraged.

Increase Support for R&D-Intensive SMEs: To maintain the UK’s competitive edge in innovation, the government could revisit the tax relief system and introduce targeted incentives for R&D-intensive SMEs.

Align R&D Incentives with Industrial Strategy: To maintain the openness of the R&D tax scheme, the government could stimulate innovation in both traditional sectors and high-growth areas like AI, biotech, and cleantech. Expanding incentives for research and commercialisation can stimulate private-sector investment, foster job creation, and contribute to long-term economic growth.

If you are interested in reading the report please get in touch.

Find out who can claim capital allowances in the UK, and which assets and property types qualify.

A step-by-step guide to making a capital allowance claim in the UK.

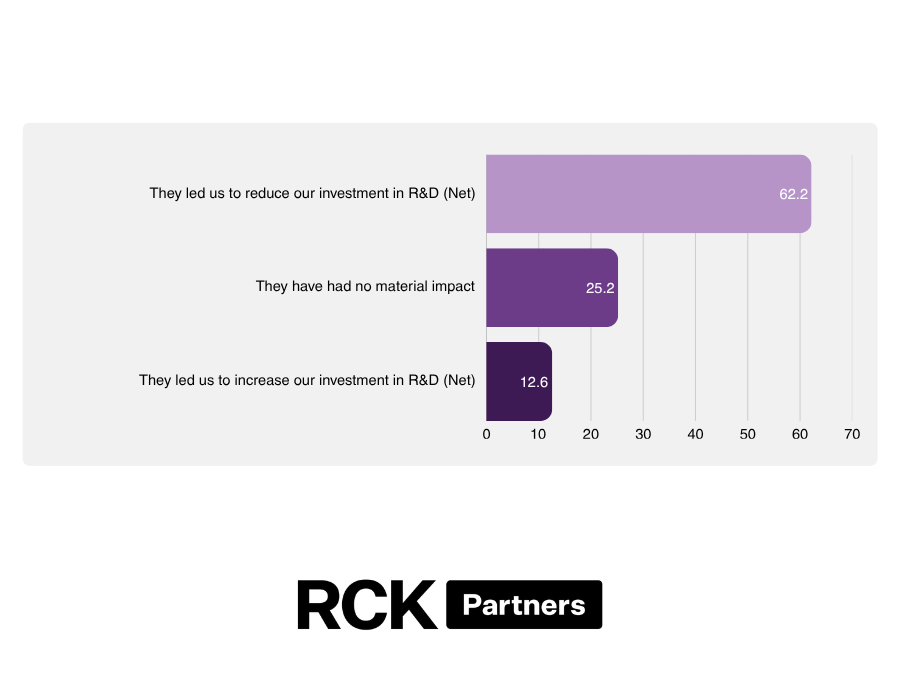

A Times-featured study, commissioned by RCK Partners and conducted by Censuswide, suggests that recent reforms to the UK's R&D tax relief scheme may have gone too far. The research found that measures introduced by HMRC to tackle abuse of the scheme are having unintended consequences for genuine innovators, with many businesses reporting that they have cancelled research initiatives, paused investment plans and reduced skilled headcount as a result of increased uncertainty surrounding the regime.