%20(4).png)

Contact

Find us

- RCK Partners,

70 Gracechurch Street,

London,

EC3V 0HR.

© 2024 RCK Partners - Company House No: 12396021

Last updated: June 2026

We sat down with Rufus Meakin, Senior Advisor and Brand Ambassador at RCK Partners, to discuss the classification of R&D subcontracting. Rufus has worked in innovation funding and the wider R&D incentives market for 25 years and regularly writes on R&D tax relief, innovation policy and HMRC compliance.

The classification of R&D subcontracting ownership remains a highly debated and complex aspect of R&D tax credit claims and has historically led to confusion among claimants.

In many cases, entitlement to R&D tax credits for subcontracted R&D activity depends on which party intended or contemplated that R&D would be undertaken when the contract was entered into. While the company commissioning the work may often have the stronger entitlement, the specific facts and circumstances of each arrangement remain important.

· Entitlement to R&D tax relief does not automatically follow either the company commissioning the work or the company carrying it out.

· HMRC considers which party intended or contemplated that R&D would be undertaken when the contract was entered into.

· Contracts remain important, but HMRC will also consider the surrounding circumstances, including how the parties behaved in practice.

· Contemporaneous evidence, such as specifications, emails and project documentation, may help demonstrate who intended the R&D and which party has the stronger entitlement to claim the relief.

· Businesses should ideally review contractual and commercial arrangements ahead of the project commencing rather than waiting until an R&D claim is being prepared.

It is understood that few areas of R&D tax credits continue to generate as much confusion as subcontracted R&D. The complexity of the issue is reflected in HMRC's recently launched Advance Assurance pilot, where entitlement to relief for subcontracted R&D is one of the specific questions that eligible businesses can ask HMRC to consider before submitting a claim.

Often businesses assume that entitlement can be determined simply by identifying who paid for the work or who carried it out, but the reality is often more complex. Recent Tribunal decisions and subsequent HMRC guidance have reinforced the importance of looking beyond contractual wording and considering how an arrangement operated in practice. Under the merged scheme, HMRC's focus is on whether the R&D was intended or contemplated when the contract was entered into, having regard to the contract and the surrounding circumstances. As a result, businesses need to look beyond who performed the work and consider who anticipated that R&D would need to be undertaken in the first place.

Under the merged scheme, a company can generally claim relief for qualifying expenditure on R&D that it contracts out to another party. The legislation and HMRC guidance focus on whether it was reasonable to assume that R&D was intended or contemplated when the contract was entered into and awareness that R&D may take place is unlikely to be enough to qualify. HMRC now expect a more specific appreciation of the R&D being undertaken. In simple terms, HMRC is seeking to identify which party recognised that an advance in science or technology would be required, and commissioned work on that basis.

This does not necessarily mean that the company carrying out the technical work will be entitled to claim. In many cases, the company commissioning the work may be the party with the stronger entitlement. The objective behind the reforms is to reduce situations where multiple parties seek relief for the same underlying expenditure. Providing greater clarity around entitlement has been along standing aim of HMRC's approach to R&D tax relief. To illustrate this, the following simplified examples show how entitlement may sit with different parties depending on the facts and circumstances of the subcontracting arrangement.

A manufacturing company engages an engineering consultancy to develop a new production process that requires overcoming significant technical uncertainties.

The manufacturer identifies the technical objectives, anticipates that R&D will be required and remains involved throughout the project. Project specifications, tender documentation and internal records all indicate that the manufacturer expected R&D to be undertaken from the outset.

In those circumstances, the manufacturer may have the stronger entitlement to claim relief, even though much of the technical work is undertaken by the consultancy.

A company engages a software developer to deliver a new business system but specifies only the desired outcome rather than the technical approach.

The software developer determines how the solution will be designed and developed, assumes responsibility for over coming the technical challenges involved and undertakes additional R&D beyond the scope originally envisaged by the customer.

In those circumstances, the contract or may have the stronger entitlement to claim relief for the R&D it undertakes.

One of the most important developments under the merged scheme is the emphasis placed on evidence surrounding the arrangement.

HMRC will not typically look solely at the wording of a contract. It will also consider the wider commercial context and how the arrangement operated in practice.

Relevant evidence may include:

· The contractual terms agreed between the parties

· Technical specifications and project scopes

· Tender documentation

· Feasibility studies and proof-of-concept work

· Project initiation documents

· Internal correspondence and emails

· Records of technical meetings

· Evidence of supervision and oversight during the project

Taken together, these documents help establish whether R&D was anticipated from the outset and which party intended it to be undertaken.

It’s important to note that the provided examples and conditions are not exhaustive. While every case depends on its specific facts, certain features may support the position that a company intended or contemplated R&D when entering into an arrangement.

Examples include:

· Project specifications or tender documentation indicating that technical uncertainties would need to be addressed

· Evidence that the company anticipated the need for R&D before entering into the arrangement

· Ongoing involvement in technical decision-making or project governance

· The subcontracted activities forming part of a wider programme of R&D being undertaken by the company

· Internal records, emails or meeting notes demonstrating that R&D was expected from the outset

· Commercial arrangements that reflect the undertaking of exploratory or feasibility work, rather than simply the purchase of a finished product

None of these factors is determinative in isolation. HMRC is likely to consider the overall picture so seeking specialist advise is important who can advise on this ahead of time.

Not every arrangement will result in entitlement sitting with the customer.

There may be circumstances where a contractor undertakes R&D independently and for its own purposes.

Factors that may support this view include:

· The customer specifies the desired outcome but not the technical route required to achieve it

· Responsibility for solving technical challenges rests primarily with the contractor

· The contractor retains significant freedom over methodology, design decisions and development activities

· Commercial risk sits predominantly with the contractor

· The contractor retains intellectual property arising from the work (although IP ownership alone does not determine entitlement).

· The contractor undertakes additional R&D beyond the scope originally envisaged by the customer

These situations require careful analysis and cannot be determined by reference to any single contractual clause.

Many businesses associate R&D tax relief with technical reports, project narratives and scientific or technological uncertainty. Whilst those elements remain important, the subcontractor reforms have increased the significance of the documents that exist before a claim is ever prepared. Contracts, statements of work, tender documents and project initiation records can all play a key role in demonstrating who intended the R&D and why it was undertaken.

For finance teams, this means that some of the most valuable evidence may sit outside the tax function and may have been created months or even years before a claim is submitted.

Businesses that commission or undertake R&D should consider reviewing:

· Whether contracts accurately reflect the nature of the work being undertaken

· How technical objectives are documented at the outset of a project

· Whether project records clearly demonstrate the need for R&D

· How technical oversight and decision-making responsibilities are allocated

· Whether intellectual property provisions align with the commercial reality of the arrangement

· What supporting evidence is retained throughout the life of the project

Addressing these questions early can help reduce uncertainty when preparing future claims.

The subcontractor reforms were introduced to provide greater clarity around entitlement and to reduce the risk of duplicate claims. The practical effect is that businesses must now pay closer attention to the circumstances surrounding an arrangement, not simply the technical work that was ultimately performed.

Although HMRC has made a clear effort to define boundaries in what has long been a contentious area, the classification of expenditure as being subcontracted/subsidised, or not, will ultimately depend on the specifics of each individual case.

For many organisations, the most important evidence may no longer be found solely in technical reports. Contracts, project documentation and records of commercial decision-making are increasingly central to demonstrating entitlement under the merged scheme.

Understanding the need for increased and wider documentation is likely to become an increasingly important part of preparing robust and defensible R&D tax relief claims.

No. The subcontractor reforms are intended to reduce situations where multiple parties seek relief for the same underlying expenditure. However, this does not necessarily mean that only one party can ever claim under a contractual arrangement.

In some circumstances, both parties may be able to claim relief where they incur qualifying expenditure on separate R&D activities or projects, and each satisfies the relevant legislative requirements for its own expenditure.

For example, a customer and contractor may both undertake their own separate R&D activities within a wider commercial relationship, but they cannot both claim relief for the same underlying expenditure.

No. HMRC will also consider the surrounding circumstances, other documentation and records and the behaviour of the parties.

A contractor may still be able to claim for R&D undertaken independently and outside the scope originally contemplated by the customer.

Not necessarily. Intellectual property ownership is one factor HMRC may consider, but it is rarely determinative on its own.

Not necessarily. HMRC will consider the contract alongside the surrounding circumstances, including project documentation, correspondence and how the arrangement operated in practice.

Businesses should retain contemporaneous evidence such as contracts, specifications, statements of work, project plans, emails chains and records of technical discussions. This can help demonstrate who intended the R&D and why it was undertaken.

Find out who can claim capital allowances in the UK, and which assets and property types qualify.

A step-by-step guide to making a capital allowance claim in the UK.

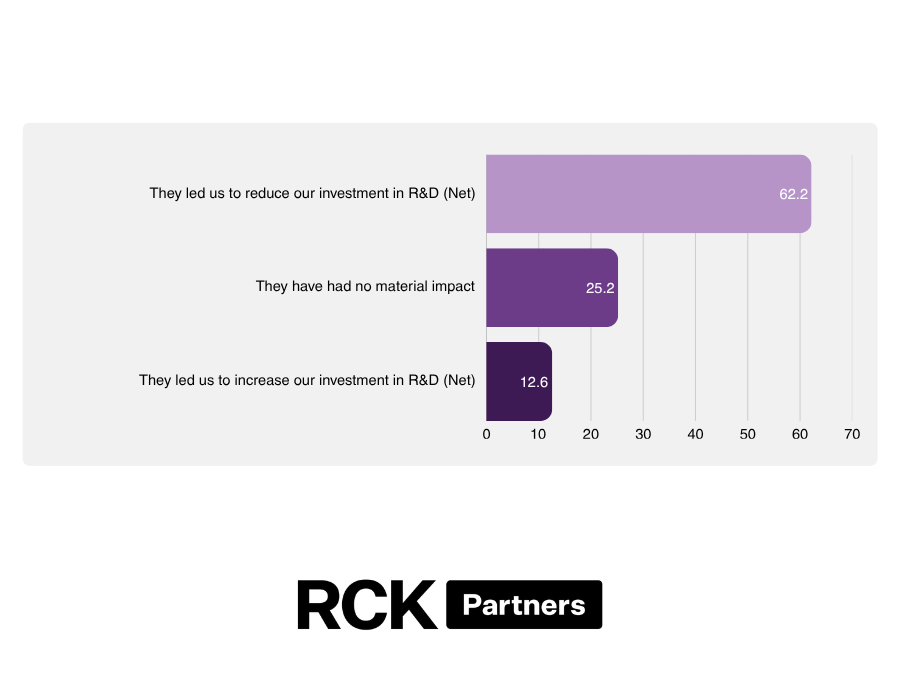

A Times-featured study, commissioned by RCK Partners and conducted by Censuswide, suggests that recent reforms to the UK's R&D tax relief scheme may have gone too far. The research found that measures introduced by HMRC to tackle abuse of the scheme are having unintended consequences for genuine innovators, with many businesses reporting that they have cancelled research initiatives, paused investment plans and reduced skilled headcount as a result of increased uncertainty surrounding the regime.