%20(4).png)

Contact

Find us

- RCK Partners,

70 Gracechurch Street,

London,

EC3V 0HR.

© 2024 RCK Partners - Company House No: 12396021

.jpg)

We spoke with Anastasiya Kokonova, Capital Allowances Partner at RCK Partners, to break down full expensing capital allowances.

In this Q&A, we explore what full expensing is, which assets qualify, how it differs from other capital allowances such as the super deduction, and how businesses can ensure they are maximising available relief across property, refurbishment, and capital investment projects.

1. What assets qualify for Full Expensing tax relief in the UK?

Full expensing capital allowances allow companies to claim 100% tax relief in the year expenditure is incurred on qualifying new and unused plant and machinery. This includes assets such as manufacturing equipment, machinery, fixtures, data cabling, office fit-outs and certain commercial building systems.

However, not all expenditure qualifies. Special rate assets, such as integral features including heating, ventilation and air conditioning systems, do not qualify for 100% full expensing, although they may qualify for the separate 50% first-year allowance.

There are also important exclusions, including second-hand assets, leased assets, and expenditure on building structures. This is where specialist review becomes important, as many refurbishment and construction projects contain a mix of qualifying and non-qualifying expenditure that requires detailed analysis.

2. How much tax can a company actually save through Full Expensing?

One of the main advantages of capital allowances full expensing is the immediate corporation tax saving it generates.

For example, if a company invests £1 million in qualifying main pool plant and machinery and claims full expensing, the company can deduct the full £1 million from taxable profits in year one. Based on a 25% corporation tax rate, this could generate a tax saving of up to £250,000.

Similarly, a £400,000 commercial fit-out project containing qualifying equipment could potentially generate tax savings of £100,000 where full expensing applies.

This accelerated relief significantly improves cash flow compared to claiming writing down allowances over many years.

3. What’s the difference between AIA, WDA and Full Expensing for Capital Allowances?

Businesses often ask: what is full expensing and how does it differ from other capital allowances reliefs?

The Annual Investment Allowance (AIA) provides 100% relief on qualifying expenditure up to the annual limit and is available to most businesses.

Full expensing explained simply means that companies can claim unlimited 100% relief on qualifying new and unused main pool plant and machinery expenditure incurred from 1 April 2023 onwards.

Writing Down Allowances (WDAs), by contrast, spread tax relief over time at either 14% or 6% per annum depending on the asset category.

The most beneficial relief depends on the type of expenditure, ownership structure and timing of investment, which is why tailored advice is often essential.

4. Can property renovations and fit-outs qualify for Full Expensing?

Yes, many commercial property renovations and fit-out projects contain qualifying expenditure eligible for full expensing capital allowances.

Typical qualifying items may include commercial kitchens, data cabling, specialist equipment, sanitaryware connected to plant systems, and other qualifying fixtures within offices, hotels, warehouses, care homes and industrial facilities.

However, structural elements such as walls, floors, roofs and general building fabric do not qualify and instead may fall under Structures and Buildings Allowance (SBA).

Detailed cost analysis is therefore critical to maximise the amount qualifying for immediate relief.

5. What mistakes do companies make when claiming Full Expensing?

A common issue is failing to identify all qualifying expenditure within wider construction or refurbishment costs. Many businesses either underclaim or incorrectly allocate qualifying assets into non-qualifying categories.

Other frequent mistakes include:

Without detailed review, significant tax relief opportunities can easily be overlooked.

6. Can Full Expensing be claimed alongside other capital allowances reliefs?

Yes, full expensing can often be claimed alongside other reliefs within the same project.

For example:

This means a single commercial development or refurbishment project may involve several different capital allowances treatments, requiring careful analysis to maximise relief.

7. How do you identify hidden qualifying assets in a commercial property purchase or refurbishment?

Many qualifying assets are embedded within construction and not separately identified within contractor accounts or financial records.

Specialist capital allowances reviews involve analysing:

Site surveys are also often essential to identify qualifying plant and machinery that may otherwise be missed. This is particularly important in commercial property acquisitions, refurbishments and large-scale fit-out projects.

8. What evidence and documentation does HMRC require for a Full Expensing claim?

To support a compliant claim, businesses should retain detailed supporting documentation including invoices, construction contracts, fixed asset registers, specifications and cost breakdowns.

HMRC may also require evidence that:

Accurate documentation is essential both for maximising relief and reducing HMRC enquiry risk.

9. Why should companies use a specialist capital allowances advisor for Full Expensing claims?

Full expensing explained in legislation is relatively straightforward, but identifying qualifying expenditure in practice can be highly technical.

Specialist capital allowances advisors help businesses:

In many cases, detailed specialist analysis can uncover substantial additional qualifying expenditure that would otherwise be missed through standard accounting reviews alone.

10. Why should companies use a specialist capital allowances advisor for Full Expensing claims?

Full expensing explained in legislation is relatively straightforward, but identifying qualifying expenditure in practice can be highly technical.Specialist capital allowances advisors help businesses:Identify hidden qualifying assets. Maximise up front tax reliefEnsure compliance with HMRC legislationReduce the risk of underclaiming or errorsAccelerate tax savings and improve cash flowIn many cases, detailed specialist analysis can uncover substantial additional qualifying expenditure that would otherwise be missed through standard accounting reviews alone.

11. Who are the best advisers for claiming full expensing capital allowances?

The best advisers are specialist capital allowances consultants with experience in commercial property, construction, and HMRC legislation.

At RCK Partners, our team includes chartered surveyors with specific expertise in capital allowances, enabling us to identify qualifying plant and machinery within complex property and refurbishment projects, maximise tax relief, and ensure full HMRC compliance.

Using a specialist team like ours often results in significantly higher claims compared to standard accounting treatment alone.

Find out who can claim capital allowances in the UK, and which assets and property types qualify.

A step-by-step guide to making a capital allowance claim in the UK.

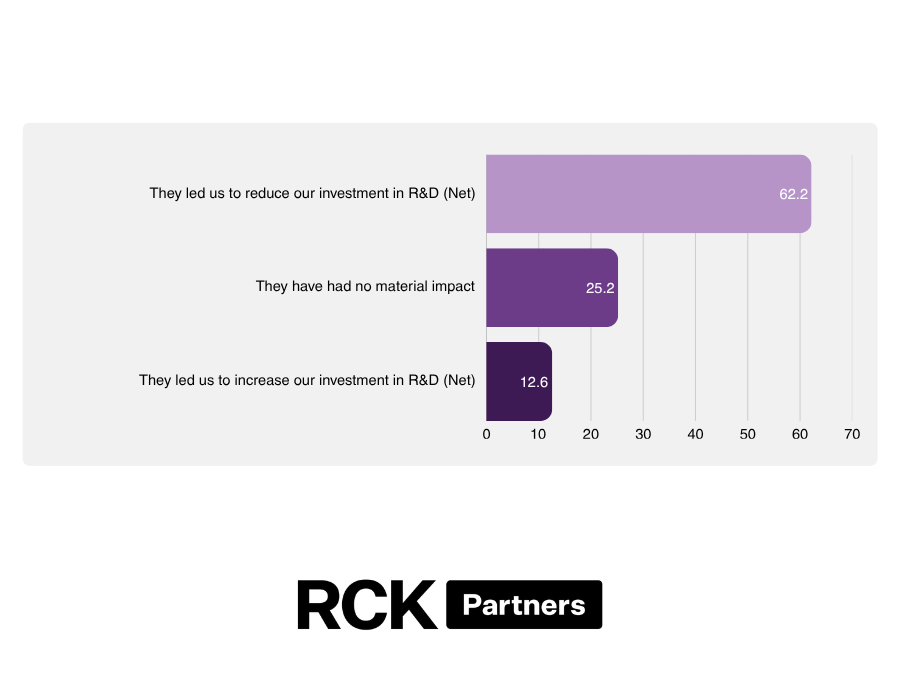

A Times-featured study, commissioned by RCK Partners and conducted by Censuswide, suggests that recent reforms to the UK's R&D tax relief scheme may have gone too far. The research found that measures introduced by HMRC to tackle abuse of the scheme are having unintended consequences for genuine innovators, with many businesses reporting that they have cancelled research initiatives, paused investment plans and reduced skilled headcount as a result of increased uncertainty surrounding the regime.